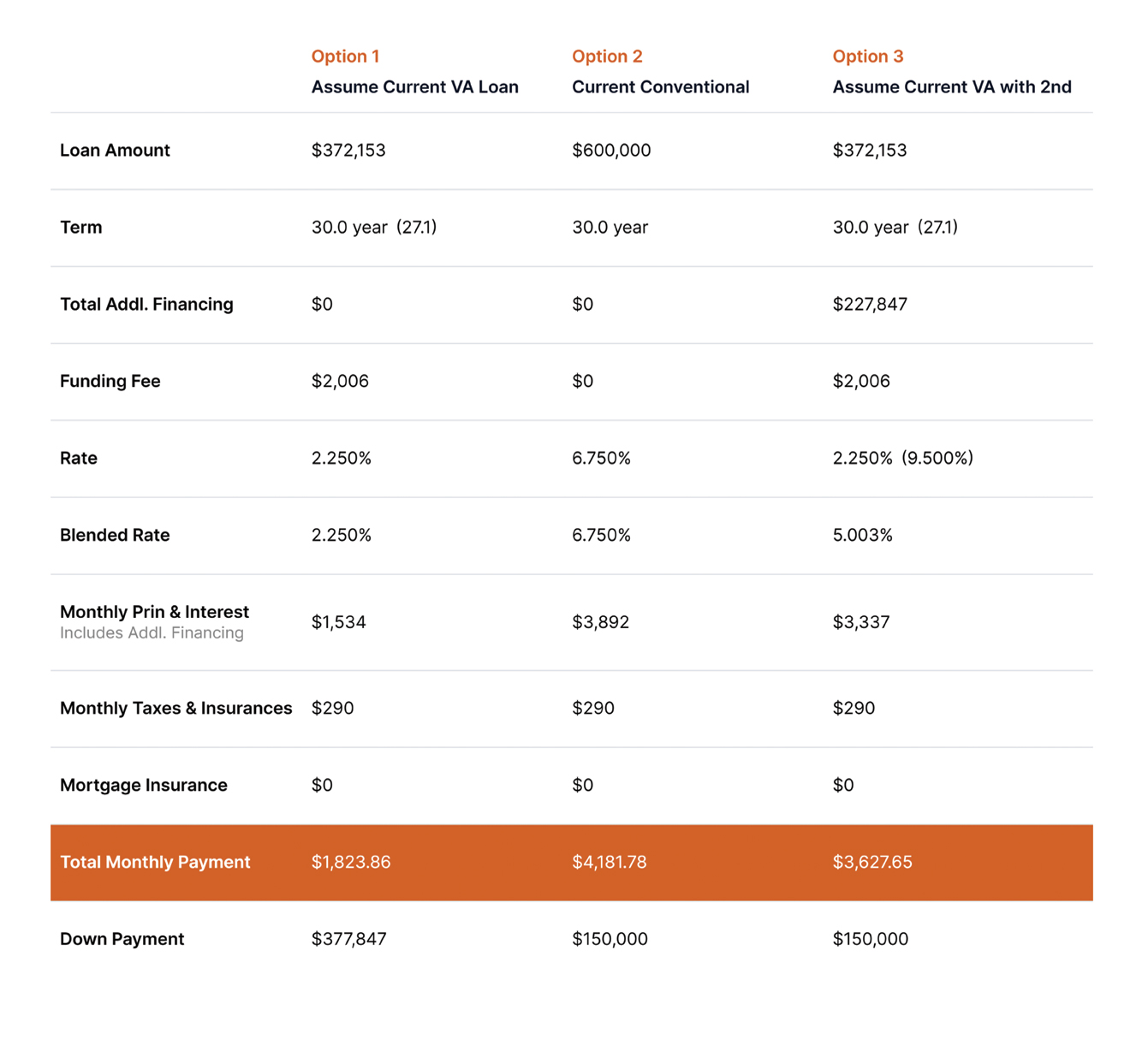

In difficult real estate markets, buyers and sellers (and their agents) are always trying to find a way to make their listing or their offer stand out against the competition. In hot sellers markets, buyers write love letters to the sellers and offer all sorts of concessions like letting the seller stay in the home after closing, or they’ll put exorbitant amounts of non-refundable earnest money down if their offer is accepted, waive inspections, etc. In tougher, more buyer driven markets like we’re in now, sellers will often offer to pay for a buyer’s closing costs or buy their interest rate down. One advantage that only certain sellers have now that is proving to be a very big selling point, is allowing a buyer to assume their current loan, which means the buyer would also benefit from their historically low interest rate. This is nothing new and is entirely legal and above board, but we haven’t seen the use of loan assumptions in a very long time because for the last 40 years interest rates have been trending down, not up. Now that rates are back in the 7% range, however, buyers are mighty interested in a seller’s 2 or 3% rate and are motivated to do what it takes to get it. If you look at the side by side comparison chart below, which is a real life example of a VA assumable loan, you can see the tremendous advantage to assuming the current loan terms.

It is important to note that assumable loans are only possible with government insured loans like VA and FHA, which combined make up a little less than a quarter of the current mortgages in the Phoenix area. The process is quite a bit different from a normal sale and can take considerably longer to close (usually 70-90 days). Buyers and sellers have some important factors to consider before deciding to go down this road and should educate themselves by speaking to an assumption specialist. When done correctly, a seller will be fully released from their liability on their loan, and a veteran will regain their entitlement so long as another veteran assumes the loan. Buyers will have to find a way to pay for the difference between the current loan and the purchase price, but there are potential financing options for that and those can be discussed with a lender.

If you are looking to potentially sell your home in the near future and have an FHA or VA loan, please give me a call and I’ll fill you in more about the process, pros and cons, and can connect you with our preferred assumption specialists to go over all of your important questions. Or, if you’re looking to sell and don’t have an assumable loan but still have questions, give me a call. I’d love to talk nerdy with you :)