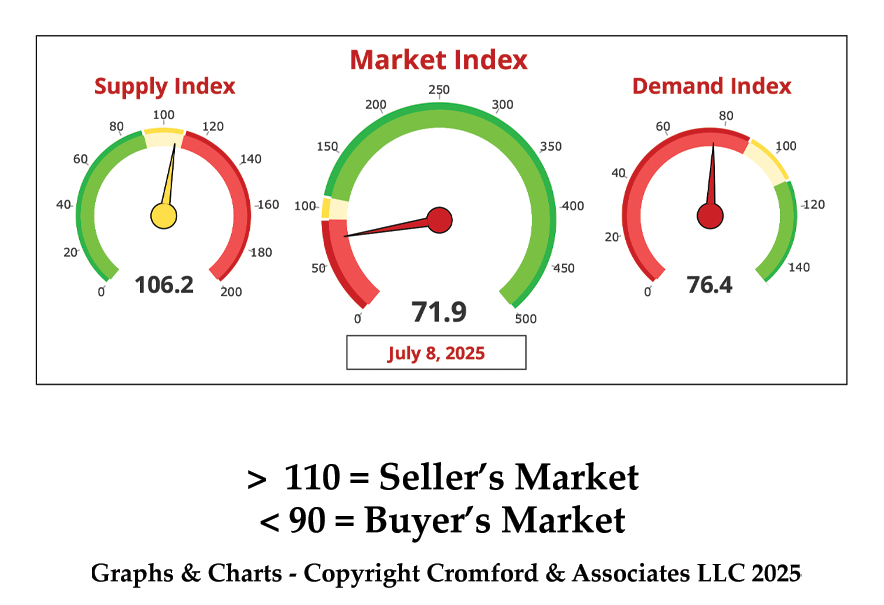

Over the past few years, and especially the past few months, I have written about the ongoing trend of increasing supply and diminishing demand, and consequently the softening home values. Last month, I wrote about the difference between a buyer’s market and a seller’s market, explaining that we’re in only the fourth buyer’s market in the last nearly three decades. I have also said many times that the current market is dramatically different than the crashed market of the early 2000s. One glaring difference between now and then is the sheer amount of distress in the market during those early years. Bank owned and short-sale properties were the predominant sources of the dramatically oversupplied market. Many people were either going through this themselves or knew someone who was actively losing their home. This market, by contrast, has been challenging, sure… but the vast majority of homes for sale are traditional, straightforward listings. With these listings, the seller has more than enough equity to pay off the mortgage, and in most cases has enough proceeds left over to buy another home.

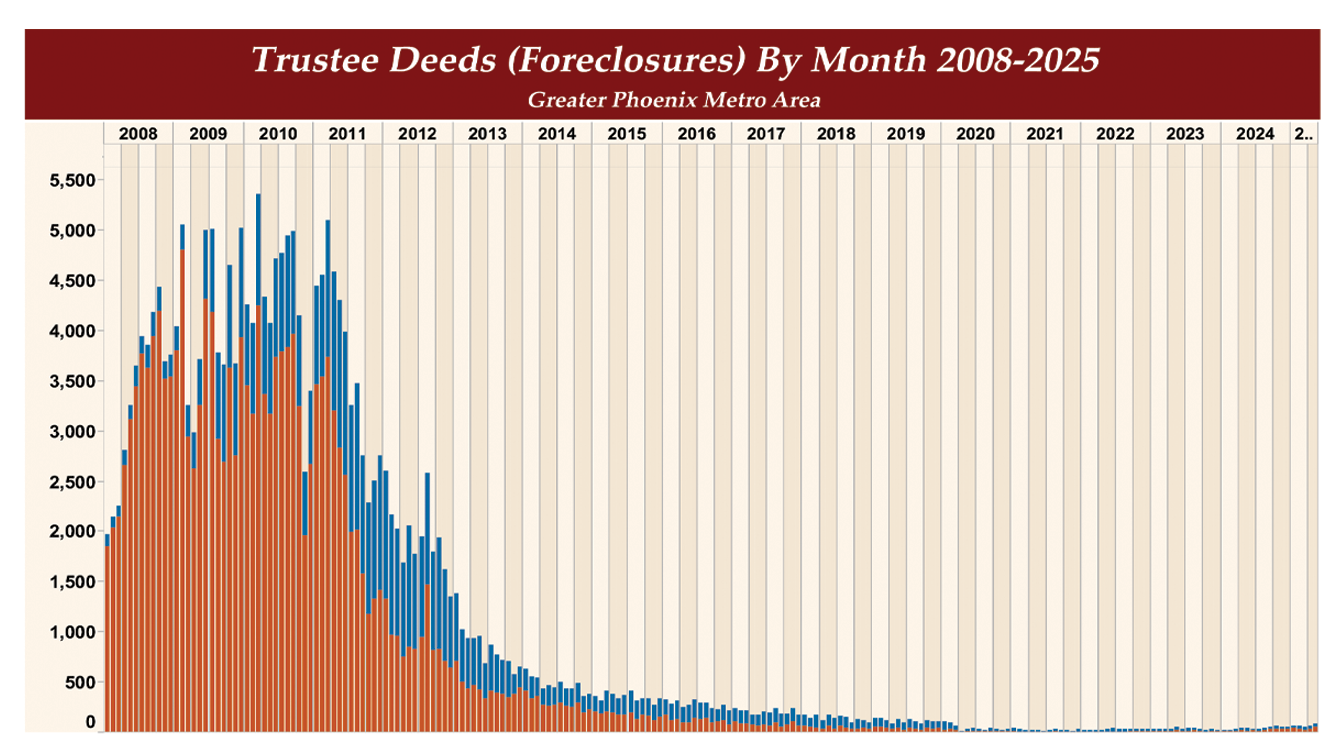

In this month’s newsletter, I would like to address the topic of distressed sales directly because, while still a very small percentage, the increase over the last few years is notable. When evaluating any particular data point, it’s important to recognize that the change over any given period of time can be more revealing than the actual number itself. For example, in the month of May, there were 389 new Notices of Trustee Sale issued, which is the notice given prior to foreclosure. This number may or may not sound like a lot, and is, in fact, quite low by long-term standards; however, it is up from 315 in May of 2024, which is an increase of nearly 25%. After the homeowner is notified of the Trustee Sale, the clock has officially started for the home to be foreclosed on and sold at auction. In May, there were 73 Trustee Sales, which is the highest number of foreclosures since before COVID. To again keep everything in its proper perspective, there were 4,000+ foreclosure auctions happening every month between 2008 and 2011. It is abundantly clear that the current market doesn’t begin to compare to those dreadful years, but we’re discussing the topic again today simply to point out that foreclosures are on the rise again, and it’s worth continued attention. Overall, mortgage delinquency remains very low, but car loans and credit cards are seeing much higher rates of default, and that gives some cause for concern.

The majority of prospective sellers we meet with today have enough equity to sell, but we are beginning to see signs of trouble for a handful of those we meet with. If someone is in financial distress and is unable to pay their bills, they may need to sell their home to stay afloat. If they bought their home at the peak of the market in late 2021-2022, however, it could be challenging to sell their home today without taking a significant loss. In this case, they may end up being forced into a short sale, which is where a home sells for less than the amount owed on the mortgage. This is a lengthy process, and it can be difficult, stressful, and also requires lender approval. If the lender does not approve the sale and the homeowner can’t pay their mortgage and catch up on their delinquent payments, they may then be forced into foreclosure. Again, as I said above, the overwhelming majority of sales happening today are still traditional equity sales, and nothing suggests we will see anywhere close to the level of distress we saw during the crash. That being said, it is my sincere hope that everyone reading this newsletter is doing okay financially, but if you’re worried about yourself or someone you know and would like to talk about your specific situation, please give me a call. I’d love to talk nerdy with you :)