It’s that time again, when we are far enough into the year (six weeks as of this writing) to start seeing the beginnings of a few important trends. Specifically, we want to assess the number of new listings coming to market, which is the supply side of the equation. While I do intend to briefly discuss demand, we’ll focus primarily on supply this month for a few reasons. In a market with weak demand like we’ve seen for the last several years, supply can quickly reach surplus levels. Additionally, a notable rise in new listings this early on could signal potential seller optimism, which is also worth exploring.

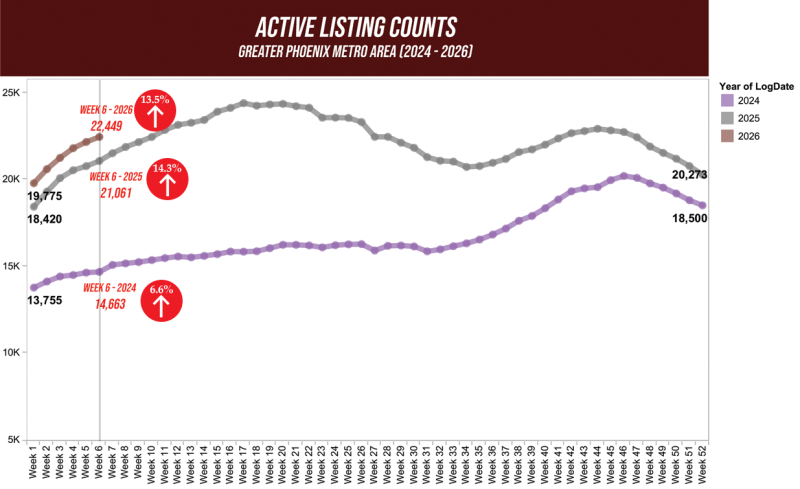

In the graph below, we’ve compared active listings in 2026 to the previous two years, which helps us evaluate the trend. So far this year, we’ve seen a 13.5% increase in the first six weeks, compared to 14.3% in the same period last year. This is a marginal improvement, but given that we started the year off with a baseline of 1,355 more listings, it’s an important one. 2024, by comparison, had a much quieter start with only a 6.6% increase. As I said in last month's newsletter, these data points only give us a snapshot of the current moment, but they don’t necessarily predict how the rest of the year will play out.

For example, in 2025, the rapid rise in new listings leveled off in late April, and the year ended with roughly the same amount of inventory as it began. In contrast, 2024 ended about 35% above where it started. So if the six-week trend isn’t indicative of the rest of the year, why does it even matter, you might ask? The answer to that again comes back to balance, and it’s why we can’t talk about supply without also talking about demand. One would think that the drop in mortgage rates over the last several months would have buyers more excited about purchasing, but that hasn’t quite materialized yet for whatever reason. It could, however, be a factor for sellers, as they might believe the lower rates would give them a better chance of selling this year… thus giving rise to more listings.

Listings under contract are slightly above the previous two years, which is good, but not at quite the rate necessary to burn through the accumulating supply. Looking at the market index, we can see that the Phoenix Metro market is still in a buyer’s market (below 90), and unless something changes considerably with either supply or demand, we will likely remain in a buyer’s market come springtime. With that being said, I will stress what I said last month. There is still reason to be hopeful that the overall market is remaining stable and could even be on the mend. The median sales price for February is $455k, only $5k lower than last year this time. Also, as I mentioned above, mortgage rates are a full percentage point below last year this time.

Market corrections can take years to fully come out of, and during this period, we must continue to pay attention to what the data is telling us. The market must stabilize before it can return to normal, and I believe there are a number of metrics that indicate that this is where we are. Don’t get me wrong, these aren’t the most exciting times to buy or sell a home, but they’re also not “bad times”. It will probably take longer, and more negotiation will be required to sell a home than most sellers would prefer, but a good, well-priced home will sell. So, if you’re considering selling your home anytime in the near future and would like to discuss your options, please give me a call. I’d love to talk nerdy with you :)