It seems that just about every year, there is someone out there claiming that the world is going to end on some remarkably specific date and time. They’re so absolutely sure of this, and they make fantastical claims about the conspiracies to cover up the truth. They want so badly for people to believe what they’re saying, but of course, without any meaningful evidence. So, why do I start here this month? Because this same level of catastrophizing and fear-mongering happens when it comes to the housing market, and it’s wise to question what we hear and read. There’s always another Chicken Little predicting another major collapse that is going to be as bad as, if not far worse than any previous economic disaster ever seen. Based on what, exactly, we should ask.

These types of claims are not only outrageous they are also wildly unfounded. Yet, they often sound legitimate because they are usually shrouded in big numbers, use big words, and are disguised as “facts”. Since many news outlets want clickbait and flashy headlines, they carry and spread these stories, lending undue journalistic credibility to these contrarian YouTubers and pundits, who, I might add, have made these provocative claims year after year without even once being proven correct. Nick Gerli, for example, a YouTuber with over 670k subscribers, has predicted a massive reduction in home values every year, without fail, since 2018. If at first you don’t succeed, as they say… So, today, I want to address this kind of misinformation that spreads across the internet and to provide some real-world data and pragmatic insight that will hopefully assuage any anxiety or concerns brought to you by the Bad News Bears.

In the last few weeks, one prediction in particular has come up that was the catalyst for this month’s topic. This prediction, made by another YouTuber named Melody Wright, is that the national housing market could see a 50% reduction in home values in 2026, claiming that it will be far worse than 2008. After Melody published her video, she was then quoted in Newsweek and MSN, and was interviewed by several other outlets to talk about and expound upon her forecast. She cites reasons such as what she calls the “new subprime crisis”, or FHA loan delinquency, excess housing supply caused by investors, unaffordability, and even the dying off of the Baby Boomer generation. Melody also predicted this would happen in 2025, but since it didn’t, we’ll try to treat it as though the goalpost was simply moved to next year.

There is far too much to unpack here in everything she said, but with video headlines like “Worse than 2008” and “Built-to-Ruin”, Melody is sure sounding the alarm. Her 50% collapse in home values prediction is the one that especially caught the attention of many, so let’s address that. First, to put into context just how severe a 50% reduction in home prices would be, let’s look at the worst our country has ever seen. In 1930, the lowest year of The Great Depression, with unemployment at a staggering 25%, home prices saw an annual decline of about 18%. For a time more of us can remember, from 2008 to 2009, home prices fell nationally by 18.9%. While some cities like Phoenix and Las Vegas were, indeed, hit much harder than others, this is a far cry from the 50% national depreciation Melody is predicting. I think it’s fair to say that if she were to be correct, there would be a few bigger issues to worry about than home values.

There is far too much to unpack here in everything she said, but with video headlines like “Worse than 2008” and “Built-to-Ruin”, Melody is sure sounding the alarm. Her 50% collapse in home values prediction is the one that especially caught the attention of many, so let’s address that. First, to put into context just how severe a 50% reduction in home prices would be, let’s look at the worst our country has ever seen. In 1930, the lowest year of The Great Depression, with unemployment at a staggering 25%, home prices saw an annual decline of about 18%. For a time more of us can remember, from 2008 to 2009, home prices fell nationally by 18.9%. While some cities like Phoenix and Las Vegas were, indeed, hit much harder than others, this is a far cry from the 50% national depreciation Melody is predicting. I think it’s fair to say that if she were to be correct, there would be a few bigger issues to worry about than home values.

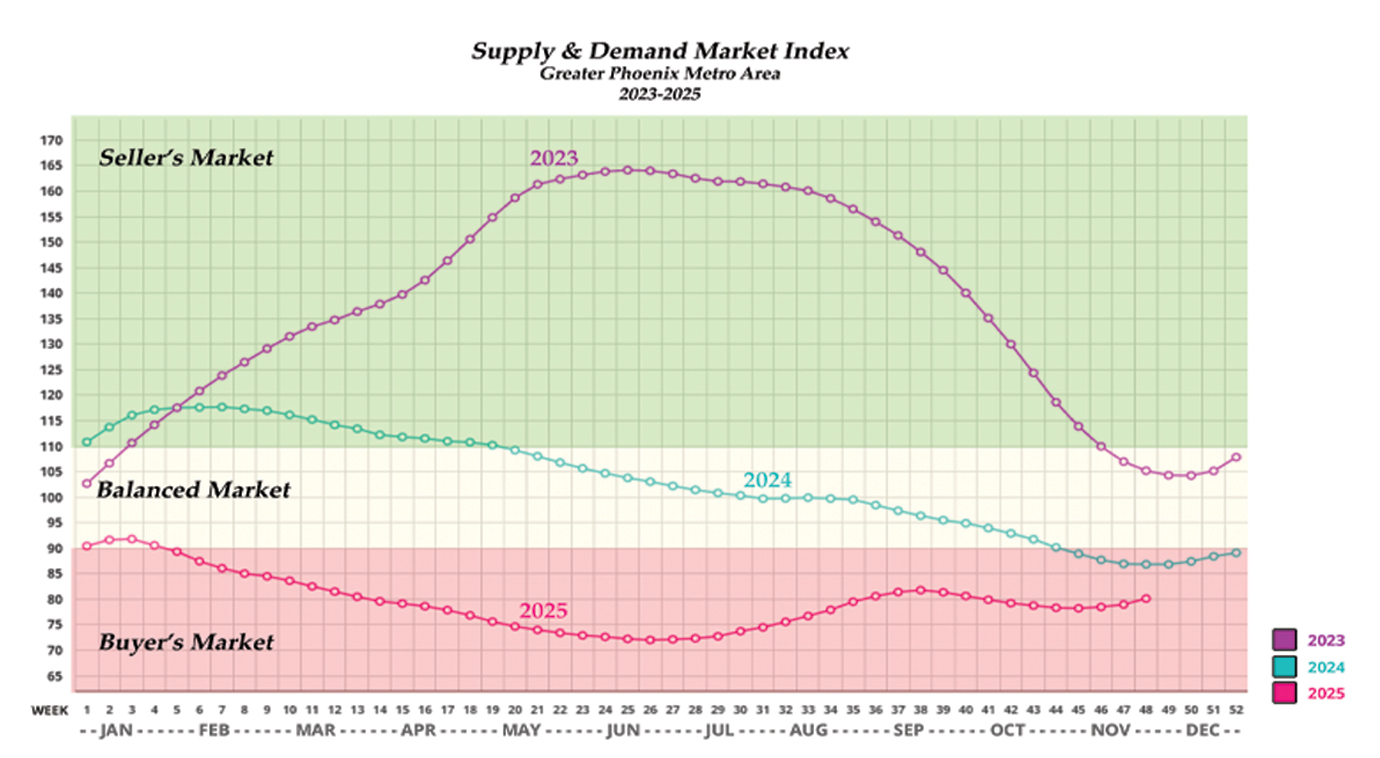

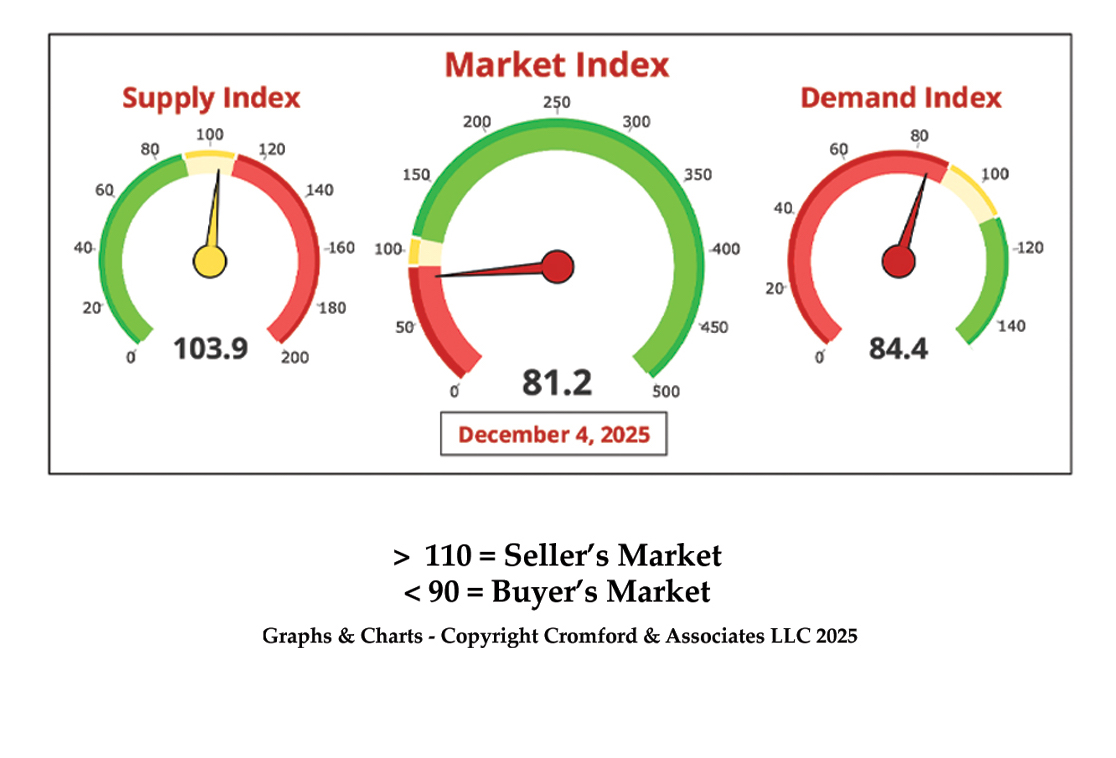

In the graph you can see that the supply index for the Phoenix area is currently at roughly 104, which is to say, very normal levels. Demand is still low with an index at about 84, but this is actually beginning to improve a bit with the lower interest rates. The overall Market Index is 81, which is just below the balanced range. While this data is only for the Phoenix market, it still gives us a fair indicator for the rest of the nation. Rather than signs of serious deterioration, we see positive indicators, with decreasing supply and increasing demand. There is absolutely no data to suggest a hidden or forthcoming surge in foreclosure listings, despite what some might say. Mortgage delinquencies are, in fact, higher than they have been for a few years, but are still well below historic levels and certainly below 2005 levels just before the crash.

To sum this up, I want to tell you, our reader, that the most remarkable thing about our market is that it’s unremarkable. Yes, it’s a bit quiet out there in this buyer’s market, and homes aren’t as easy to sell as they once were. Most homes are definitely selling for less than they were a few years ago, and that trend may very well continue into next year. That is a correction, however, NOT a collapse. Nothing other than the voices of a few loud individuals even remotely indicates an impending crash or a doomsday scenario. Nothing. It can be easy to be swept up by scary headlines and soundbites, but this is why it’s important to question them. If things were really as bad as these people are saying, there would be a cacophony of ringing alarm bells, not just a few outlandish YouTubers warning that the sky is falling. So, if you’re thinking of selling anytime in the near future or just want to calm your nerves and talk things through, please give me a call. I’d love to talk nerdy with you :)