The topic of supply & demand is a regular theme in this newsletter, as many of you know. Something we spend less time talking about, however, is the myriad of factors that directly affect the decisions individual buyers and sellers make every single day. The decision to buy a home today or wait for better times…maybe a time that feels a little less uncertain. The decision to sell a home today, wait a few months, or perhaps even a few years. Maybe wait until there are fewer homes on the market or a time when homes are selling more quickly. Whatever the reason, there’s always something that contributes heavily to the decisions made by any one home buyer or seller. At scale, these decisions ultimately drive the balance of supply & demand, and therefore drive the market. Today, one of the most significant variables is, surprise surprise, the stubbornly high mortgage rates. Extremely low mortgage rates in the 2-3% range, like during the COVID years, made borrowing money feel almost free, and this, in turn, drove demand to near record-high levels. The other side of that particularly volatile coin is what we’ve been dealing with since 2022, when rates skyrocketed, peaking at over 8% in late 2023. This slammed the proverbial brakes on the market, and we’ve been sluggishly moving along ever since. As we’ve continued to navigate this market, it seems that many people are perpetually hoping and waiting… waiting for this thing or that thing, something that might finally break the log jam and allow rates to come back down.

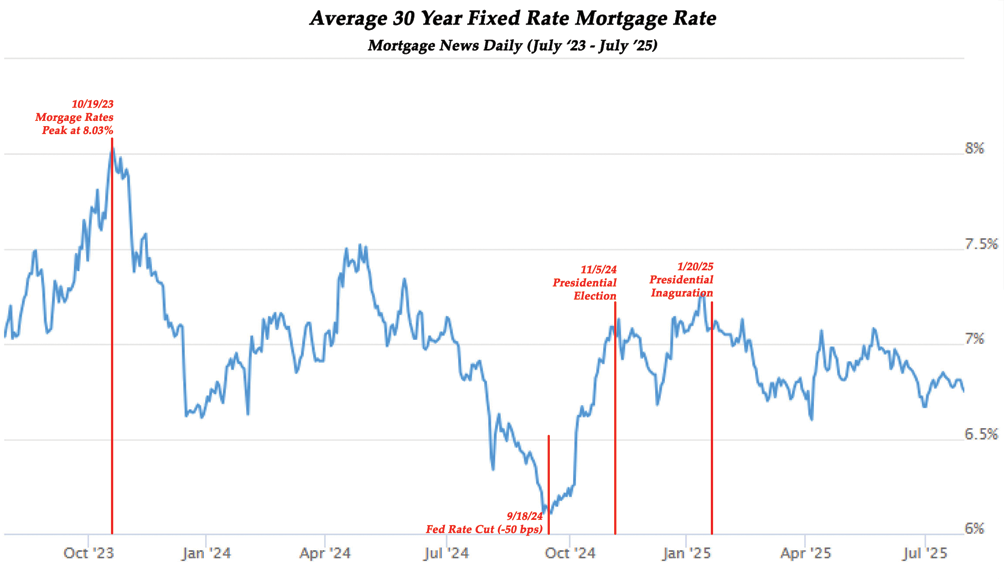

The Federal Reserve raised the Federal Funds Rate, or “Fed Rate,” seven times in 2022 and another five times in 2023. This, of course, caused mortgage rates to climb. Given that the Fed Rate is the rate at which banks borrow and loan money to each other, it makes logical sense that mortgage rates would follow. With that said, however, it doesn’t necessarily translate that a decrease in the Fed Rate will cause mortgage rates to drop. There was a lot of optimism and anticipation that the Fed would make the first rate reduction last year, which they did (3 times, in fact). If you look at the chart below, you can see that mortgage rates were rapidly declining in advance of the September 17th Fed meeting. You can also see that just following this much-anticipated drop, mortgage rates rapidly shot back up. During this time, I met with many buyers and sellers who were waiting for this date, hoping it would be the answer to their prayers, only to be dismayed when the outcome was nothing but more disappointment. Then politics aside, the presidential election was the next big thing on the “let’s wait and see” list. That date, again, came and went, and still, mortgage rates remained largely unchanged. What about the inauguration? Surely rates would drop after Trump was sworn in, right? Sadly, wrong again. And herein lies the crux of the problem. External events, good or bad, certainly CAN affect the mortgage rates, but it doesn’t mean they will or are even likely to. The Fed Rate is important, but it’s only one ingredient in the stew when it comes to the many factors that affect mortgage rates. Other factors would include inflation, which is currently 2.7% (around the same level as 2017-2019), the 10-Year Treasury Yield, which is currently 4.22%, which is about the historic norm, and the overall economic outlook, which in a weak market would typically mean lower rates.

So, what gives, you might ask? Much of the data suggests that mortgage rates SHOULD be lower, but they’re not, and it’s anybody’s guess as to when they’ll come down. I’ve been hearing expert predictions since 2022 that said “by the end of the year, rates will be back down to 5%”, then again in ‘23, ‘24, and still today. The fact of the matter is that we simply cannot predict when mortgage rates are going to come down. What we can say, however, is that until they do, many buyers are going to sit on the sidelines, waiting for them to come down. Until demand picks up, it is very unlikely that we’ll burn through enough of the excess inventory we’ve accumulated to tip back into a seller’s market. Until we’re in a seller’s market again, values will likely continue to soften, and homes will take longer to sell. Waiting is a good solution for those who have the luxury, but for those who can’t, now is the best time to buy or sell because it’s right in front of us and is the only market we really know. So, if you’re considering buying or selling and would like to discuss your specific situation, please give me a call. I’d love to talk nerdy with you :)